The Winning Formula Needed to Thrive in the New Shale Order

Resiliency, Transparency & Sustainability – a Strategic Playbook Where None Exists

By: Adnan Khan, Nicholas Carnrite & Kyle Vano

Dear 2020,

Good Riddance.

Yours Truly,

Oil and Gas Industry

Investor apathy, hesitant capital markets, and crushing debt challenged the industry long before the COVID-19 global pandemic smashed demand and crushed crude prices this year.

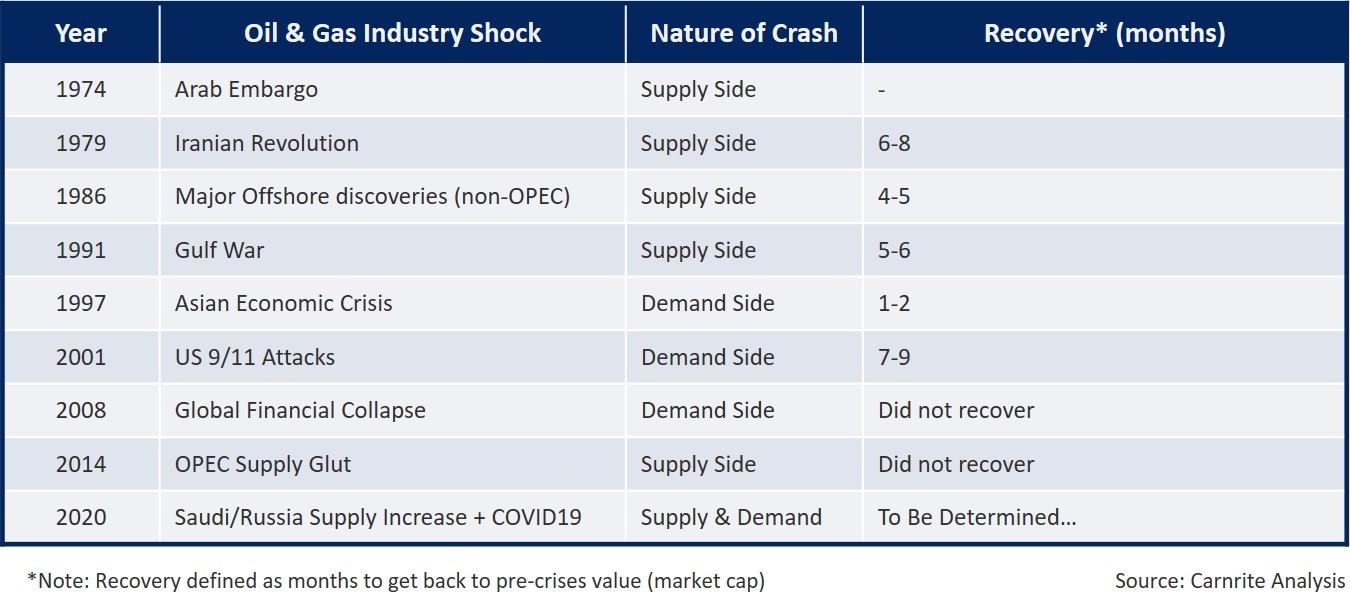

Historically, when the industry encountered challenges it was able to cut costs, defer investments and wait for the “optimistic” cyclical turnaround in oil prices. This time, things have been different, not only because of concurrent supply & demand forces at play, but also the span through which it may play out. Going back 40+ years, the majority of the shocks were induced due to sudden supply contractions in reaction to geopolitical unrest, resulting in price increases. Demand-side shocks were primarily due to macroeconomic contractions and have been closely tied to larger economic cycles. Further analysis suggests supply-side shocks are normally shorter, lasting on average 5-6 months, and less severe, compared to demand shocks which require a longer recovery period (to pre-crisis levels). In 2020, the industry was faced with simultaneous supply and demand shocks, and the true extent of the damage is, unfortunately, yet to be determined.

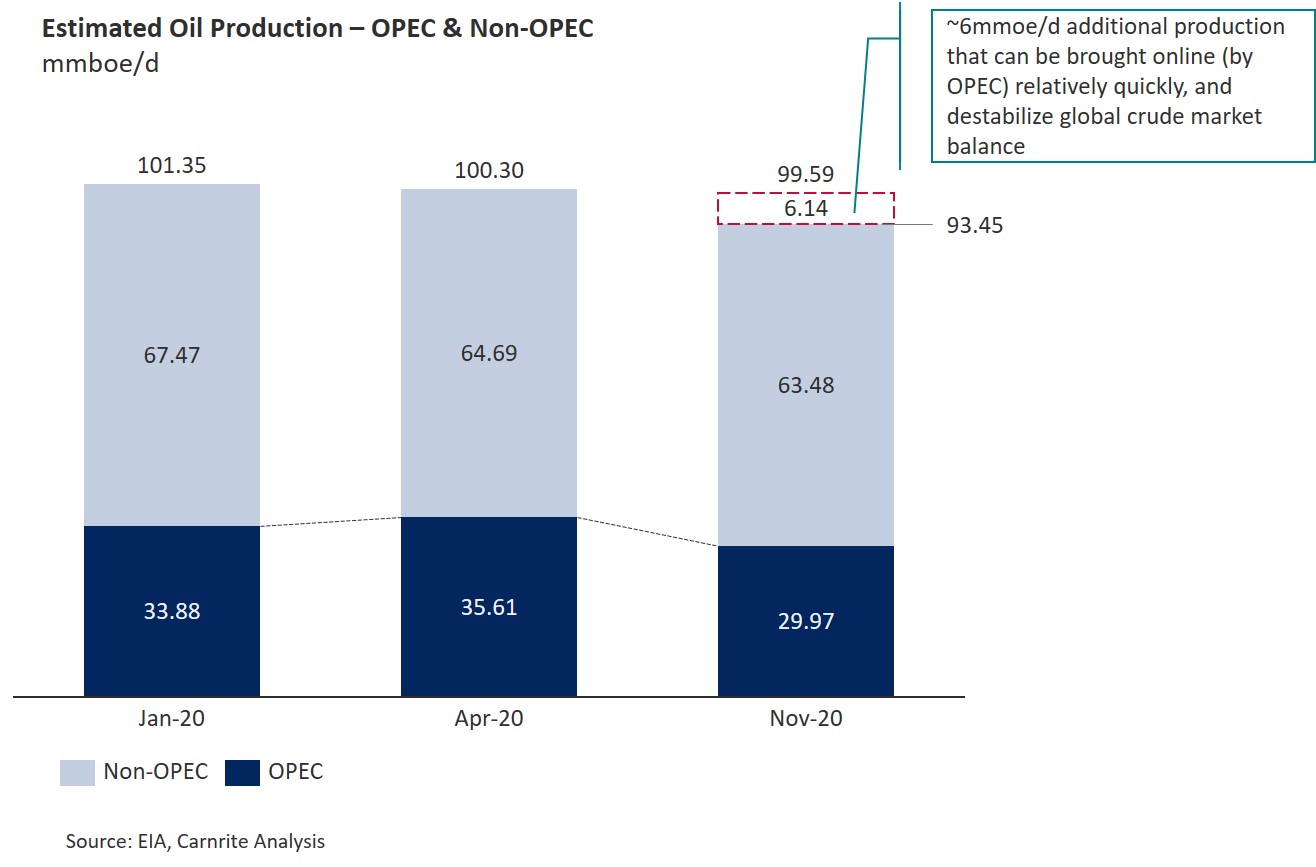

From the onset, US production has borne the brunt of the hit from the simultaneous demand contraction and supply fluctuations (in the context of a flat supply curve). Despite oil prices having recovered, after falling a dizzying 60%+ in April, the short-term outlook remains challenging (likely lasting well into 2021), as the erosion of demand caused by the COVID-19 pandemic continues to stunt an already challenged industry. Furthermore, it is worthwhile to acknowledge that OPEC continues to hold back ~6mmboe/d of collective production that can easily be brought online as demand recovers or in a renewed attempt to gain market share, which would once again destabilize the crude market (and near-term prices and industry sentiment along with it).

The medium and long-term outlook remains equally uncertain due to pressures for decarbonization, structural changes in societal habits (how we live, work, socialize, learn, shop, and experience things) reducing energy intensity, abundant energy supply availability, and continuing debt obligations.

History doesn’t repeat, but it often rhymes

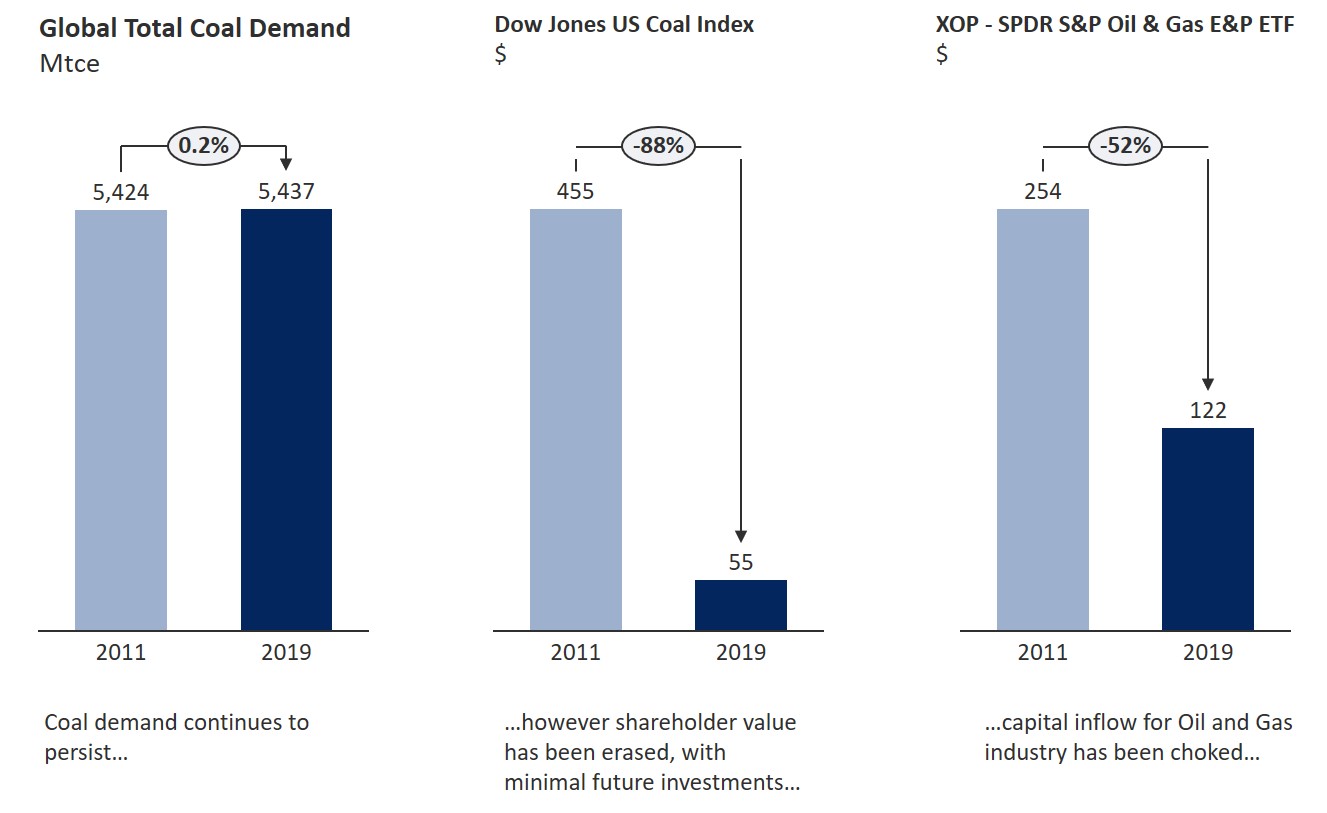

The question might not be as much about if/when the demand comes back, or what the oil price models predict for the future, but perhaps more importantly if the Oil and Gas industry can once again sustainably achieve the shareholder value it generated in decades past. The coal industry might have forewarned and painted a bleak picture for the road ahead for O&G, as the global demand for coal has declined marginally since 2011 (however, 2020 has shown the biggest drop in coal demand since World War II). Despite a surprisingly resilient demand, coal prices have decreased dramatically, capital commitments have plummeted, and the industry struggles to attract capital or access capital markets.

The future remains uncertain with multiple variables at play, but, with history as a guide, one thing remains certain the oil and gas industry will need to transition and reinvent itself yet again to survive the compression and avoid a fate unlike that of the coal industry.

A New Formula to Win

Winning going forward will require a new approach, and require executives to focus on three key themes, Resiliency, Transparency & Sustainability to respond to a fundamentally changed game.

Resiliency

US shale has proven its resiliency over and over again through a combination of multiple factors, including enhancing efficiency gains, innovation-driven customization of technology, and/or optimizing operational workflows. Our analysis suggests the current downturn will likely, once again, force US Shale operators to reinvent their ways of working to improve resiliency, with the most significant gains coming from leveraging digital tools and technologies to improve visibility and productivity (targeted solution designing) as well as a continued relentless focus on sustainable cost-takeouts.

(Re)Balance portfolio and capital spend

Oil and Gas operators should “unwrap” their entire asset portfolio and get down to pad/well level details to understand the true profitability of each well (based on well-level economics and analytics). Doing so provides the visibility needed to “re-wrap” the portfolio and determine which wells to shut in, what assets to keep, and where/ how new assets fit into the overall portfolio. One-way operators can quickly improve visibility into capital spending & portfolio optimization decisions is by getting a “true” LOE cost per well.

Allocate LOE costs down to well level underpinned by variable activity drivers. For example, fuel costs allocations utilizing data analytics to determine electricity consumption considering variables such as horsepower requirements, vertical depth along with battery allocation (based on total fluid production), pumper/AL expert costs allocations based on utilizing digital solutions such as GPS geofencing combined with tiered management by exception prioritization.

Another tool that operators can utilize are decision tree analytics to enable strategic planning teams to evaluate multiple strategic options across various scenarios (for example merger potential, PDP acquisitions vs inventory vs blowdown scenario) and weigh them against each other on a NAV basis) and balance the yield of upside payoff with downside risks. In the past, unfortunately, downside risks were predominately neglected in decision analysis, leading to ‘production at all costs’ outcome that destroyed significant amounts of capital in down cycles.

(Re)Establish an operational baseline to a lower demand profile

Cost-cutting isn’t new to the industry. Since 2014 operators have constantly been in one form of cost-cutting or another. The sequence of cost-cutting steps, unfortunately, remains predictable, starting with capital expenditure cuts (20%), SG&A reductions (2-3%), and supplier/vendor price negotiations (5%). This time around though, due to the structural shifts, more permanent cuts might be needed to the structure to accommodate for the new demand profile. Operators should consider a forensic-driven, laser-focused approach, starting with a blank sheet of what is needed to run the business rather than starting with what they have today. A “Should-Be” approach to cost structure enables the business to truly correlate needs to (variable) activity drivers and be able to adjust accordingly. Two areas where we have seen operators making significant savings have been on the G&A (backoffice) and production OPEX fronts, with savings resulting up to 15% (excluding any price negotiations)

Transparency

Oil and gas operators are facing intense investor scrutiny of new capital investments due to a recent history of capital destruction. In many cases this has led to inherent distrust of management teams as a result of misaligned performance metrics and disproportionate (executive) bonus payouts. Additionally, a growing number of investors are adopting policies that are placing capital at risk for companies that don’t meet environmental social and governance (ESG) guidelines and demanding oil and gas operating companies to disclose their carbon footprint along with some (active) mitigation plans. We believe that this trend will continue to persist, and that the broader sustainability push will require a steady movement towards a carbon net-neutral energy system with meaningful actions that start with methane emission tracking. Executives can focus on two priorities to improve transparency and rebuild investor trust.

(Re)Define performance metrics to align with current market context and operational backdrop

Going forward, winning companies will redefine their corporate performance management structure across the organizations down to the field and aligning metrics to various stakeholders (including investors, board and executive management teams) and revised objectives and priorities. With increasing shareholder sentiment around reducing carbon footprints, these metrics will need to incorporate carbon intensity measures.

Example: Bifurcating producing assets (PDP) and development assets with separately defined metrics with appropriate normalization unit (ie per production BOE, % EBITDA, or simply free cash flow) and integrating the metrics into a lookback process, that is utilized in a structured executive review process for business decisions. Thus, accurately capturing and reviewing total lifecycle costs (Sunk costs and go-forward economics only paint half the picture).

Deploy Carbon Footprint Management

To start the decarbonization journey, complying with investor demand and truly operationalizing ESG aspirations, we believe, operators need to start with the basics and first define a carbon baseline to understand the “True Carbon Footprint” of their assets, including pads/wells/ facilities along with corporate HQs and vehicle fleets and then link with corporate goals/targets, before moving to identifying decarbonization opportunities across Scope 1, 2 & 3. This approach would provide the visibility and transparency in defining optimization strategies for the business.

Sustainability

The energy industry has been in a state of transition since early human history starting with the earliest energy sources of wood to coal to oil, and the yet-to-determined future energy mix. Previous transitions were primarily characterized by the shortage of one energy source being replaced by another abundant energy source that provided superior benefits in the form of higher energy density, lower cost of development, and the overall betterment of society (by providing heat, light, and mobility). In contrast, the current transition we are witnessing, is perhaps, unique from the pace at its occurring, the stakeholders involved that are demanding action (both external and internal to the incumbent industry), the environmental impact consciousness (that goes beyond short-term financial gains), and the future energy mix itself.

Defining the path on the energy transition strategic game-board

Fortunately, the oil and gas operators of today have multiple strategic options to consider in the energy transition along the decarbonization and sustainability path. And while no single path is wrong in its own, the imperative is to develop the strategy and the roadmap to achieve the ambition, based on capabilities and future aspirations. Carnrite analysis has identified four distinct options to help executives define a starting point to develop a baseline:

In Conclusion

Any of the actions described as part of Resiliency, Transparency, or Sustainability in this article will provide a competitive edge, but the real winners will be those that pursue all three strategic priorities in symphonic play – either on their own or by establishing key partnerships within and across the energy ecosystem.